Is Your PropTech Strategy Truly Optimised?

How Technology Strategy Became Business Strategy in the Institutional Living Sector

Author: Wan Aqib, Global Real Estate Analyst, GAA Living

Executive summary

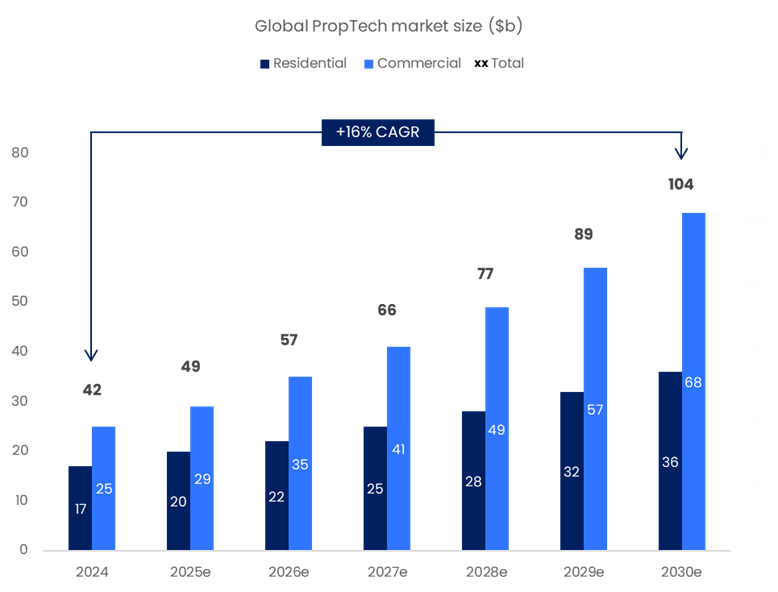

The institutional rental housing sector has undergone a structural shift in which technology has moved from back-office overhead to a primary driver of income growth, efficiency and competitive positioning. At the centre of this sits the Property Management Software (PMS) platform, which connects leasing, payments, compliance, maintenance, resident engagement, accounting and reporting into a single operating environment, functioning as the operating system of the building. The global PropTech market, valued at $42 billion in 2024 and projected to reach $104 billion by 2030, is consolidating around fewer, larger companies whose products become so embedded in daily operations that replacing them would be genuinely disruptive.

Every operator scaling a portfolio faces the same core decision: build your own technology, partner with an established vendor, or assemble a hybrid of specialist tools –a choice shaped not by IT preferences but by business model, cost structure and competitive position. Underpinning all of it is data governance, because automation and AI do not fix bad data, they amplify it. The systems and practices being put in place today will determine which operators hold a lasting edge over the next decade.

This paper provides additional context on the current global PropTech landscape, including strategic approaches and associated risk considerations.

Introduction

Not long ago, the industry ran on spreadsheets, paper leases and a patchwork of disconnected systems that few people thought twice about. That world is disappearing. In its place, a new operating reality has taken hold, one built on digital infrastructure that touches every part of the business –from how portfolios are managed and residents experience their homes, to how investors are provided with the report and how operators compete for capital and customers.

Technology in this sector is no longer a support function tucked away in an IT department. It has become a primary driver of income growth, efficiency and competitive positioning across institutional rental portfolios. The organisations that have recognised this early are pulling ahead, and those that have not are already starting to feel the gap.

This shift is being powered by a growing ecosystem of purpose-built technologies known collectively as PropTech, the application of digital tools across the full lifecycle of a real estate asset. These are not generic software solutions borrowed from other industries. They are technologies designed specifically for the built environment, covering everything from investment and development through to leasing, operations and ongoing asset management.

PropTech has deeper roots than many people realise. It began in the 1970s with basic digital tools, gathered pace in the 2000s as listings and data moved online, and has since matured into a global industry. The pandemic accelerated things further, reinforcing the shift toward digital transactions, remote engagement and technology-led property management in ways that would have taken years to unfold under normal circumstances. Research from Oxford (Sad) Business School defines PropTech around three core functions:

Information, covering data, analytics and insight.

Transactions, encompassing leasing, financing and payments.

Management, involving the day-to-day operation, optimisation of assets and the experience of those who occupy them.

What matters is that PropTech is not a single market. Some technologies support one-off activities like transactions or development, while others enable the continuous, daily operation of real estate as a business. This distinction is important because the greatest depth of software integration and value creation sits within operational and management-focused technologies, where real estate generates recurring income and measurable outcomes.

For decades, property management technology sat quietly in the background, treated as a cost centre the operations team dealt with while the rest of the business focused on deals and strategy. That era is over. In the modern living sector, spanning student accommodation (PBSA), co-living, build-to-rent (BTR) — covering multifamily and single-family rentals — and later living, the technology stack has moved to the centre of the operating model. It underpins how portfolios are run, how residents interact with their homes, how investors receive performance data and how operators position themselves in increasingly competitive markets.

A maturing market, consolidating fast

According to Fortlane Partners, the global PropTech market was valued at approx. $42 billion in 2024 and is projected to reach $104 billion by 2030, growing at around 16% a year. Between 2012 and 2023, the United States attracted $241 billion in PropTech investment –more than 60% of the global total according to the ESCP PropTech global trends barometer. China followed at $58 billion, then the United Kingdom at $24 billion. After that the numbers drop quickly, with Germany, Switzerland and Spain in the teens and single-digit billions spread across Australia, Canada, Brazil and India.

Figure 1 - Global PropTech market projected to reach $104bn by 2030, growing at 16% CAGR across residential and commercial segments.

Source: GAA using data from Fortlane Partners

This pattern is not random. PropTech capital flows toward markets with large institutional real estate sectors, deep venture ecosystems and clear pathways to scale. A country can have outstanding developers and architects, but if its rental market is fragmented across small private landlords with limited appetite for digital tools, investment will stay thin. In practice, technology adoption is shaped far more by ownership structure and institutional depth than by the availability of the technology itself.

The sector has moved past its early growth phase. The days of chasing scale at all costs and raising money on promise alone are giving way to consolidation. Investors now want tech companies that generate steady income, solve a genuine problem and can demonstrate their value. The trend is toward backing fewer companies whose software becomes so embedded in daily operations that replacing it would be genuinely disruptive.

The PMS as the digital spine

Modern rental housing is an operating business, not simply a real estate asset. Running it well means coordinating asset management, on-site operations and technology, yet most organisations are still set up around older models designed for individually owned, agent-led properties. The result is a gap between strategy, operations and systems that holds back performance.

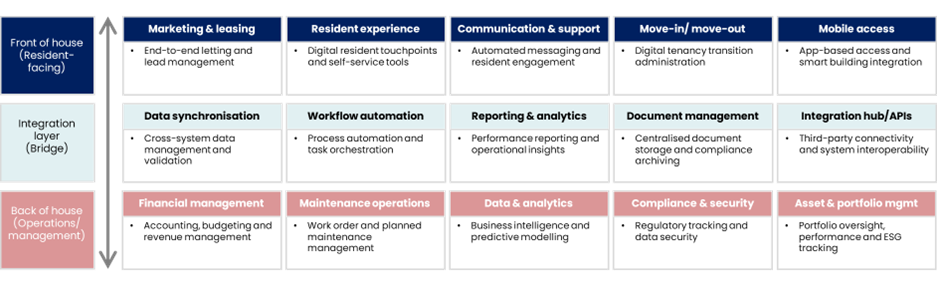

Figure 2 - End-to-end PropTech capability framework across the resident journey.

Source: GAA using data from RedChalk Group.

Note: List is non-exhaustive

Professional rental portfolios underperform not because any single function is lacking, but because operators, investors and technology systems are pulling in different directions. Platforms built for generic property management force operators to work around the software rather than with it, while poor integration and manual processes produce unreliable data that weakens pricing, forecasting and reporting. Owners often have limited visibility over their own operational data, which sits with third-party managers or vendors, and without real-time information it becomes difficult to optimise rents, occupancy and costs across portfolios. Too many core systems still operate in silos, and too many people end up doing data entry and admin instead of focusing on residents or asset performance.

This matters because there is a real difference between renting from a private landlord and renting from a professional operator. Private rental typically means multiple owners in one building, inconsistent management, reactive maintenance and older stock. Professional rental means a single accountable owner, purpose-built buildings, proactive management, better services, transparent pricing and more predictable income.

At the centre of all this sits the Property Management Software platform. The PMS connects capabilities such as leasing, payments, compliance, maintenance, resident engagement, accounting and reporting into one operating environment, acting as the digital backbone of the portfolio. When it works well, a resident can go from initial enquiry to receiving a renewal offer without leaving a single system. When it does not, operators are left juggling disconnected tools, duplicated data and manual workarounds that eat into margins and frustrate everyone involved.

Build, partner or hybrid

Every operator scaling a rental portfolio eventually faces the same core decision: do you build your own technology from scratch, partner with an established PMS vendor, or assemble a mix of specialist tools connected through APIs?

Each path has clear trade-offs. Building in-house gives you full control and ownership, but it demands serious capital and talent and effectively turns a housing operator into a software company. Partnering with a single vendor is faster and more predictable, but limits flexibility and may not work well across different markets or regulatory environments. A hybrid approach offers more agility, but introduces complexity in data management and vendor oversight that requires strong in-house technical capability to sustain.

This is not just a technology decision. It is a business model decision that directly shapes how an organisation competes, scales and delivers. Getting it wrong is expensive and disruptive. Getting it right creates a lasting operational advantage that is hard to replicate. The choice should be guided by budget, speed of deployment, internal capability, scalability, appetite for risk and how well the solution fits the way the business actually operates.

The risk and considerations

Beneath all of this sits a problem that is easy to underestimate and expensive to ignore: data quality. No PMS, AI tool or analytics platform can deliver lasting value without clean, reliable data underneath it. Automation and AI do not fix bad data, they amplify it. If the inputs are wrong, the outputs will be wrong too, whether that means inaccurate forecasts, mispriced units or dashboards that mislead rather than inform. Without proper data governance in place, every digital investment is built on sand.

Technology selection is not purely a software decision — it is a question of who owns and controls the data generated across operations. Operators must assess whether a vendor's data model allows for portability, auditability and independent access, or whether it creates dependency that limits strategic flexibility over time. As portfolio scale increases, the ability to extract, interrogate and act on proprietary data becomes a competitive advantage in itself.

Budget and total cost of ownership must be understood in full before any commitment is made. Licence fees represent only one component. Implementation, integration, training, ongoing support and eventual migration costs can collectively exceed the initial investment. Resource allocation must align with organisational priorities, and regional compliance requirements — particularly across multi-jurisdiction portfolios — add further cost complexity that is frequently underestimated at the procurement stage.

Even well-selected technology will underperform without the internal capability to implement and sustain it. Organisations must honestly evaluate existing technical skills, team readiness and management bandwidth before deployment. Integration complexity with current systems requires dedicated oversight, and the long-term operational burden on both management and front-line teams must be factored into any technology decision. A solution that exceeds the organisation's operational capacity to absorb it will generate friction rather than efficiency.

Conclusion

Rental housing now runs on a digital backbone. The PMS is the operating system, data quality is the foundation, and the choice of whether to deploy a build, partner or hybrid technology strategy is the fundamental decision. What separates the operators who get real value from technology from those who just spend money on it comes down to how well they execute. The sector is still in the early stages of professionalising at scale. The systems, structures and data practices being put in place today will shape which operators hold a lasting edge over the next decade. The window to get this right is open now, and it will not stay open forever.