Build-to-Rent / Multifamily vs. Build-to-Sell

An Asset Value Analysis in Residential Real Estate

Author: Romain Achi, Senior Director - Head of Middle East, GAA Living

Executive Summary

In this paper we explore the valuation and investment nuances between build-to-rent / multifamily (BTR) and build-to-sell (BTS), with a focus on geographies excluding the US where build-to-sell has long dominated the ‘apartment exit route’.

While the traditional BTS model has long dominated markets outside the US, BTR strategies are beginning to demonstrate superior asset value where higher rents through more professional management and sharper yields translate into higher values per square foot.

This thought piece examines how the income capitalisation approach to valuation can make BTR properties more valuable than their BTS counterparts, particularly when Net Operating Income (NOI) and capitalisation rates align to create enhanced value multiples. We illustrate this with a simplified financial model based on a typical 100-unit residential development.

In markets where rental income and yields support favourable cap rate compression, BTR assets can command valuations that exceed traditional per square foot sale prices, while simultaneously providing long-term income streams and appreciation potential that BTS models cannot capture.

The Fundamental Valuation Difference

Build-to-Sell Valuation Method

Build-to-sell assets are valued based on comparable sales methodology, where value per square foot is determined by recent sales ‘comparables’ of similar properties, market demand at point of sale, physical characteristics and finishes, and a one-time transaction price. The BTS model relies on immediate market conditions and provides a single liquidation event with no mechanism to capture future value appreciation or income generation.

Build-to-Rent Valuation Method

BTR assets are valued using the income capitalisation approach below:

Asset Value = Net Operating Income (NOI) ÷ Capitalisation Rate

This creates a fundamentally different equation to calculating value. Every £/€/$1 increase in NOI adds £/€/$25 in valuation in a 4% cap market, £/€/$20 in a 5% cap market, and £/€/$16 in a 6% cap market. This mathematical relationship means that BTR properties can achieve higher per square foot valuations when rental income is strong and exit liquidity to an ever growing institutional investor pool (seeking this type of long term stabilised income) is present.

Net Operating Income (NOI) = ‘Net Revenue’ (gross revenue less void and bad debt), minus Operating Expenditure (building operating costs)

When BTR Delivers Higher Returns

The Cap Rate Advantage

Broadly speaking, BTR as an asset class achieves capitalisation rates between 4% and 6% for stabilised investments. When the asset is well designed, well managed and its location well underwritten, the value can surpass that of a BTS asset because:

Stabilised income attracts premium valuations: Properties with steady rental income typically generate more investor interest because they represent low risk, low volatility investments.

Growth expectations: Unlike BTS properties that capture only market value at the point of sale, BTR assets benefit from expected NOI growth.

Institutional quality investments: Buyers such as Sovereign Wealth Funds, Pension Funds and Insurance Funds expect a minimum standard of asset and management quality. Well managed BTR adheres to this expected standard, adding an additional buyer universe to the mix, which increases competitive bidding.

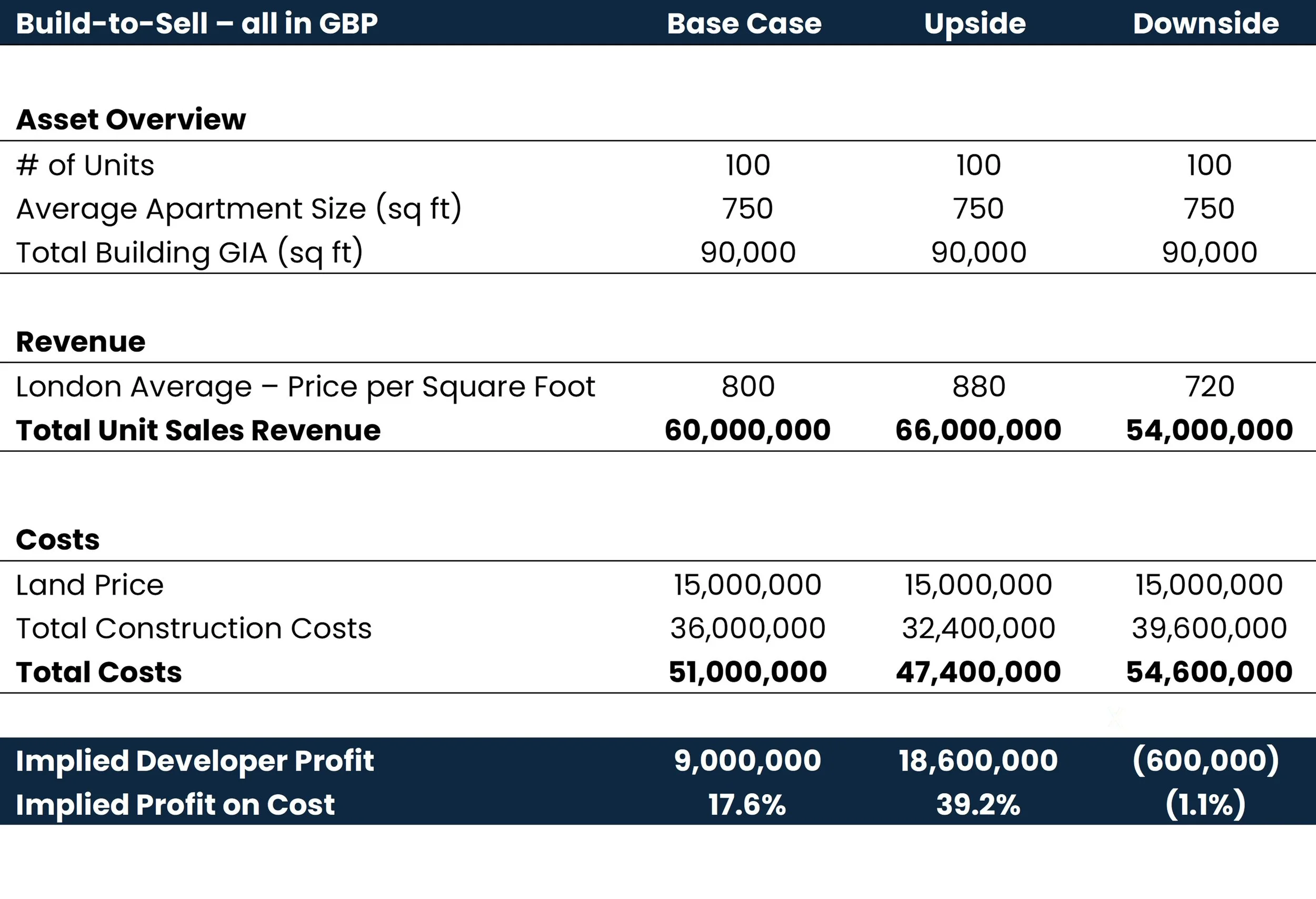

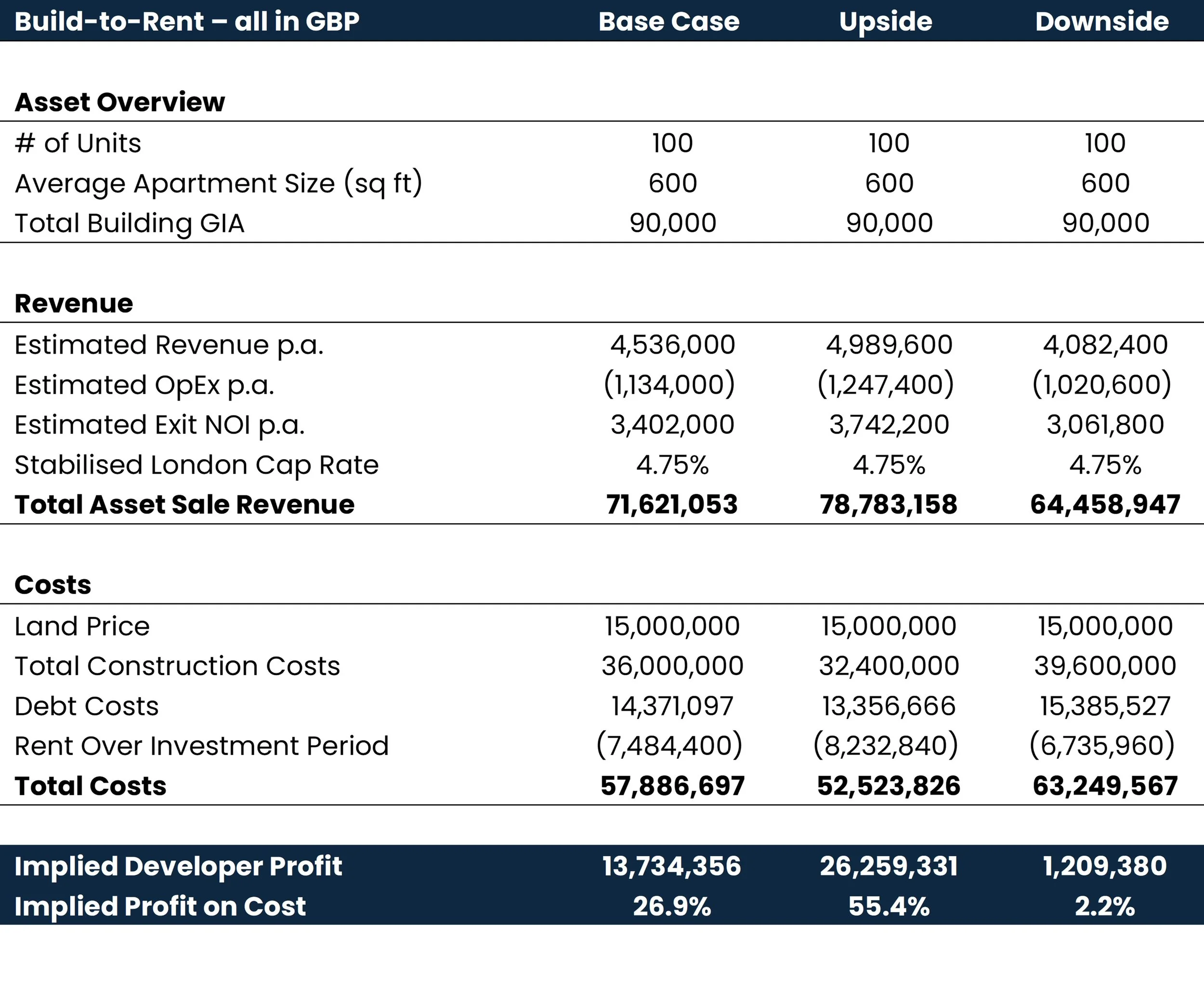

The Value Advantage: A Practical Example

The high-level calculations below demonstrate the mechanics behind BTR’s value advantage over BTS in a favourable rental market, using a like-for-like asset.

When building the valuation appraisals, it is crucial to carefully choose the assumptions factored into the BTS and BTR revenue and cost calculations. In order to ensure a fair comparison, building size, sales values, rental levels and construction costs all need to reflect the same asset in the same location.

Source: GAA Living

Source: GAA Living

Using the appropriate inputs reflecting both sales and rental levels for the same asset, we can see in the example shown above that BTR has higher profitability than BTS across scenarios, both nominally and as a percentage of cost. This dynamic applies to global submarkets where rental values and capitalisation rates are strong enough to support better returns than traditional BTS products.

GAA has developed a detailed cashflow measuring this comparison with more granularity, including differences in IRR, equity multiple and deal equity needs. Please get in touch for more information: info@GAAliving.com.

Long Term Value Creation & Risk Management

Compound Growth in BTR

Longer hold periods allows developers and investors to benefit from property value appreciation over time, especially if the asset has strong placemaking.

The BTR model offers multiple avenues for value creation:

Rental Income Growth

Market rent has increased between 15-40% on average in Europe, the US and the GCC. As shown earlier, each unit of currency increase in NOI translates into a 20x multiple to asset value (at a 5% cap rate).

NOI Margin

BTR is an active, operational asset class. This provides investors with the opportunity to improve margins through strategic asset management initiatives, further increasing NOI and asset value.

Portfolio Economies of Scale

Operating costs tend to reach a ceiling when portfolios achieve critical mass, i.e. a higher number of units under management. This allows cost to decrease on a per-unit basis over the long term, improving profitability and margins.

Tax Efficiencies

Optimising capital gains tax through depreciation and long-term financing enable BTR owners to create more efficient capital stacks. This advantage means that unlike BTS investors crystalising and paying full capital gains tax at the point of sale, BTR investors can optimise the tax burden at the point of sale.

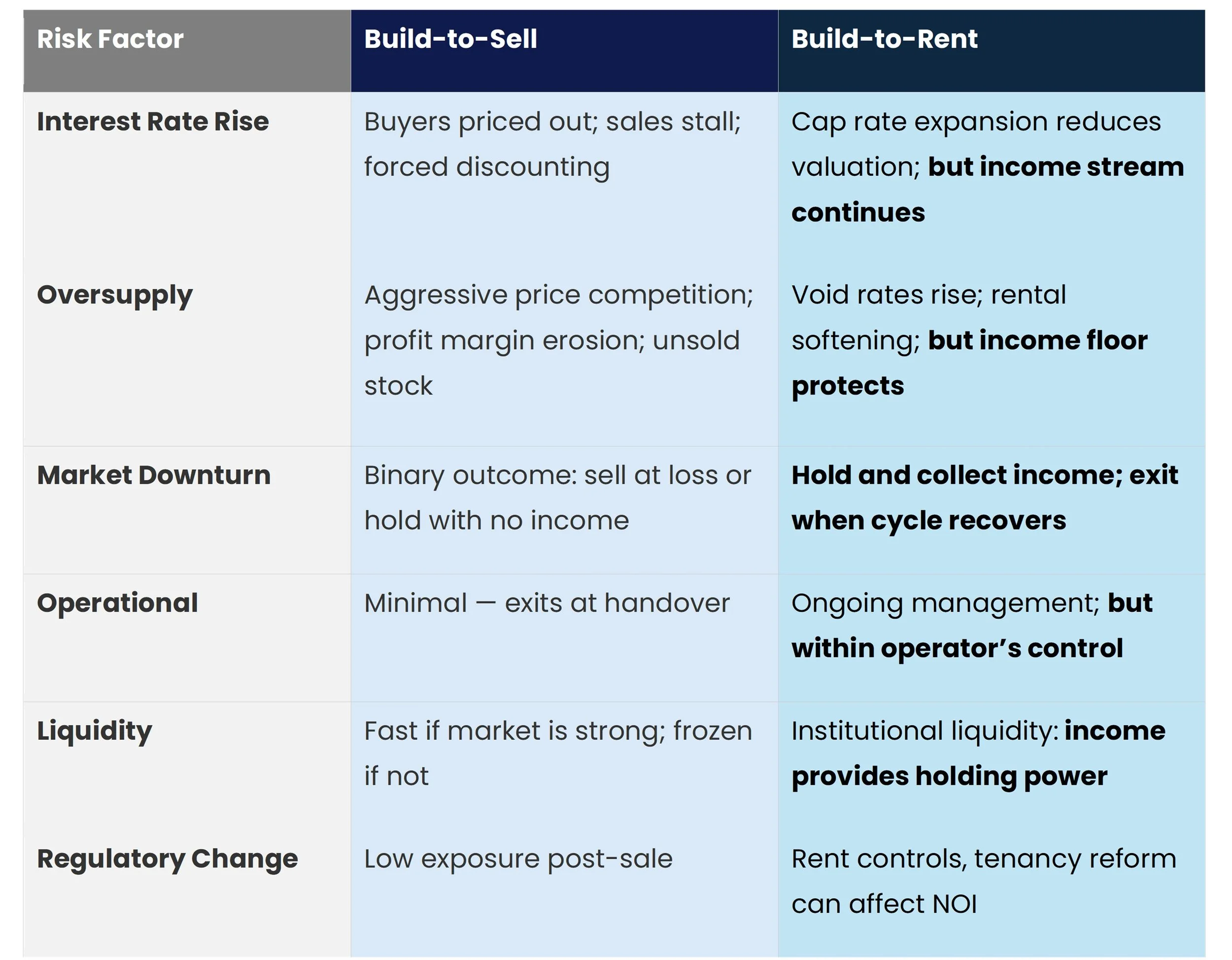

Risk Management

No investment is immune to market risk; so how do both models compare under a stressed scenario? BTR and BTS are exposed to fundamentally different risks.

Source: GAA Living

Capital Velocity

For investors keen on recycling capital in the short to medium term (close ended funds, value add investors etc), a strategy following a build-rent-sell model would suit. Stabilised assets are valued on NOI rather than sales per square foot comparables, hence a developer or investor could:

Construct and stabilise in 2-3 years

Capture rental income and tax benefits

Achieve stabilised occupancy and build an operating history

Sell stabilised asset at a premium to a BTS asset, using the NOI-based valuation

Conclusion

The analysis presented in this paper demonstrates that build-to-rent strategies can deliver materially superior returns compared with traditional build-to-sell models in markets where rental income and capitalisation rates are sufficiently strong. Across base, upside and downside scenarios, the BTR model produced higher implied developer profit, both in absolute terms and as a percentage of cost, driven by the fundamental mechanics of income capitalisation: every incremental unit of NOI translates into a significant multiple of asset value.

Beyond headline profitability, BTR offers structural advantages and downside protections that BTS cannot replicate. The ability to hold through market cycles, collect ongoing rental income during periods of volatility and benefit from compound NOI growth provides investors with a resilience that the single-liquidation nature of BTS lacks. In a downside scenario, BTS investors face the prospect of selling at a loss with no income buffer, whereas BTR investors retain a performing income stream and the flexibility to time their exit.

Furthermore, the BTR model’s operational nature unlocks additional levers of value creation; from active asset management and NOI margin improvement to portfolio economies of scale and tax-efficient capital structures that are simply unavailable to BTS developers who exit at the point of sale. For investors seeking capital velocity, the build-rent-sell strategy offers a compelling hybrid: stabilise the asset, build an operating track record, and exit at a premium valuation underpinned by proven income rather than speculative comparables.

As institutional capital continues to flow into the living sector globally, the markets that will reward investors most are those where the fundamentals of rental demand, professional asset management and market liquidity converge. For developers and investors evaluating their next residential project, the question is no longer simply whether to build, but whether to operate.